New investors know the internet holds a plethora of financial tips, some worth following – and others worth ignoring. As a physical therapist with an interest in investment and limited time to research it, how do you know which is which?

Before you follow the advice of a gutsy investor, realize there are basic rules of personal finance that you absolutely need to know. Establish solid financial systems first, and you won’t be likely to do something stupid with your money like options trading or buying a whole life insurance policy. Furthermore, a risky investment may be really appealing when you’re looking to change your financial situation quickly, but it’s not a good move.

Financial Tips For Full Financial Health

In the same way PTs examine multiple body regions during an evaluation, we need to consider the “whole body” of personal finances before investing. Financial health is not just about having “good investment skills“; it’s about coordinating a whole conglomerate of financial skills and systems.

So if you’re a physical therapist considering a fancy new investment idea you saw online, follow these financial tips first.

1. Create systems for your money

You have to start with the basics, and for many people, a budget is the first step in basic money management. However, creating (and sticking to!) a budget is only one component of a smart financial system.

I recommend YNAB, but you can start with a spreadsheet too! To optimize your financial wellbeing, you should also maintain a balance sheet, monitor your cash flow, and implement automations for your financial goals. I have videos for all of those components in the financial health playlist on my YouTube channel.

If you need help starting these systems, you can download the same worksheets I use as part of my financial bootcamp. And no, it doesn’t cost anything – I’ll email them to you for free. They’re invaluable resources that will help you create smarter systems for your money.

There are many ways to automate your savings and investments, some of which I cover in this article and elsewhere. But if you’re interested in learning even more about automating your financial life, I highly recommend you read I Will Teach You to Be Rich by Ramit Sethi. He divulges some valuable strategies for saving, investing, and increasing your wealth through automatic systems and mindful spending habits.

2. Create an emergency fund of 3-6 months

As you establish your money management systems, consider setting up an emergency fund – a stash of cash you can rely on in the event of unforeseen unemployment and hard times.

How much is enough? That really depends on a handful of factors like the number of incomes you have in your household and the volatility of your job market. Typically, a dual-income family should save at least 3 months of expenses, while a single-income household would be better off with a longer, 6-month emergency fund.

If you’re a single PT earning $65,000 a year and spending $3,000 each month, you should aim to save about $18,000 for a 6-month emergency fund.

You might be able to get away with just a 3-month emergency fund of around $9,000 if you have two income streams from a marriage or joint partnership. But if we’ve learned anything from 2020, it’s that jobs are not guaranteed, especially when you have a hands-on career like physical therapy. So, take your emergency fund seriously and fill it up as fast as possible.

3. Diversify your income

Diversifying your income simply means adding a different kind of income source into your regular stream. You can earn additional income by starting a side hustle or a business, in-person or online.

As a physical therapist, you might consider working multiple PRN jobs instead of one salaried position. Or, you can take on a weekend Home Health gig to generate extra income and pay off your student loans faster.

But if you’re tired of always having to trade hours for dollars, think outside the box; consider adding a passive income stream. What would that look like? Well, if you’re skilled in generating new ideas or presenting concepts, you can create helpful resources to sell to the public.

Going the online route will incur minimal upfront costs: for instance, you need only pay $10/year for a website domain and roughly $3/mo. for web hosting.

4. Get a Student Loans strategy

I know student loans are really annoying, and they’re probably one of the biggest expenses you have each month. But you can get rid of your student loans faster and smarter using these 3 basic steps:

- 1. Live like a student until you’ve paid off your loans.

- 2. Consider an income-driven repayment (IDR) plan for your federal loans.

- 3. Refinance your private loans to the lowest interest rate possible.

For this third step, I used and recommend Credible. By using this link, you’ll be supporting my blog and getting the lowest rate possible on your private student loans through Credible.

The Possibility of Loan Forgiveness

Barring these three strategies, you have another option in loan forgiveness, though the only plan I deem viable for physical therapists is Public Service Loan Forgiveness.

If you’re a PT with more than 2x your salary in student loans, PSLF is a great option for you – especially if your employer qualifies for the program. Beware of 20-year forgiveness plans, however, which I consider too long for PTs, not to mention the ugly tax bomb you’ll pay upon forgiveness.

By incorporating the previous tips of automating your savings and diversifying your income, you’ll be able to pay off your student loans a lot more quickly. But, you can make it even easier for yourself by refinancing private loans, applying for IDR plans and considering a forgiveness option through PSLF.

5. Pay Yourself First

A lot of times I hear PTs say, “I want to start investing, but I don’t know where to begin.” I always say, start investing in your 401k or 403b, especially if your employer offers to match it. It’s free money and your best possible return on investment (ROI). You’ll essentially be paying yourself.

Once you’ve contributed enough for your employer’s match, consider maxing out your Roth IRA. Beyond that, you can add money into an after-tax investment account, such as Vanguard or Betterment, both which I use and recommend.

A good way to save 15-20% of your income is to treat it like an expense from your first paycheck. You can set this up automatically for your 401k as well as for transfers to your IRA with Vanguard, Betterment, or most any other brokerage house.

Don’t skip paying yourself; it’s the best way to start investing. When you automate your savings and investments, you are dollar cost averaging into the market. That means, as an investor, you’ll be picking up the low days and the high days with every new contribution you make, which is one of the smartest ways to build your account over time.

It’s not glamorous investing, folks, and it’s certainly no silver bullet to swift gains. But if you embrace the pay-yourself-first mindset and invest 20% of your gross income from the start, you’ll be on a solid path to meeting your financial goals and becoming a wise investor.

If you’re still reading, I know you take your finances seriously. So the next tips cover some additional steps you can take to manage your money like a pro.

6. Speculation is NOT an Investment Strategy

Few of us can resist the appeal of huge returns and quick wealth promised by the stock market. It’s sensational – picking the winners, skipping the losers, doubling our money. Yet, even the highest-paid investment managers on Wall Street have a difficult time beating the market.

The money doesn’t come as quickly as you might think.

There’s a lot to learn about investing in mutual funds, index funds, and ETFs, much of which you can explore in the video below. But in short, instead of timing the market, focus on time in the market. Because when it comes to investing – and not speculating – long-term strategies are proven strategies, and much more worth your while.

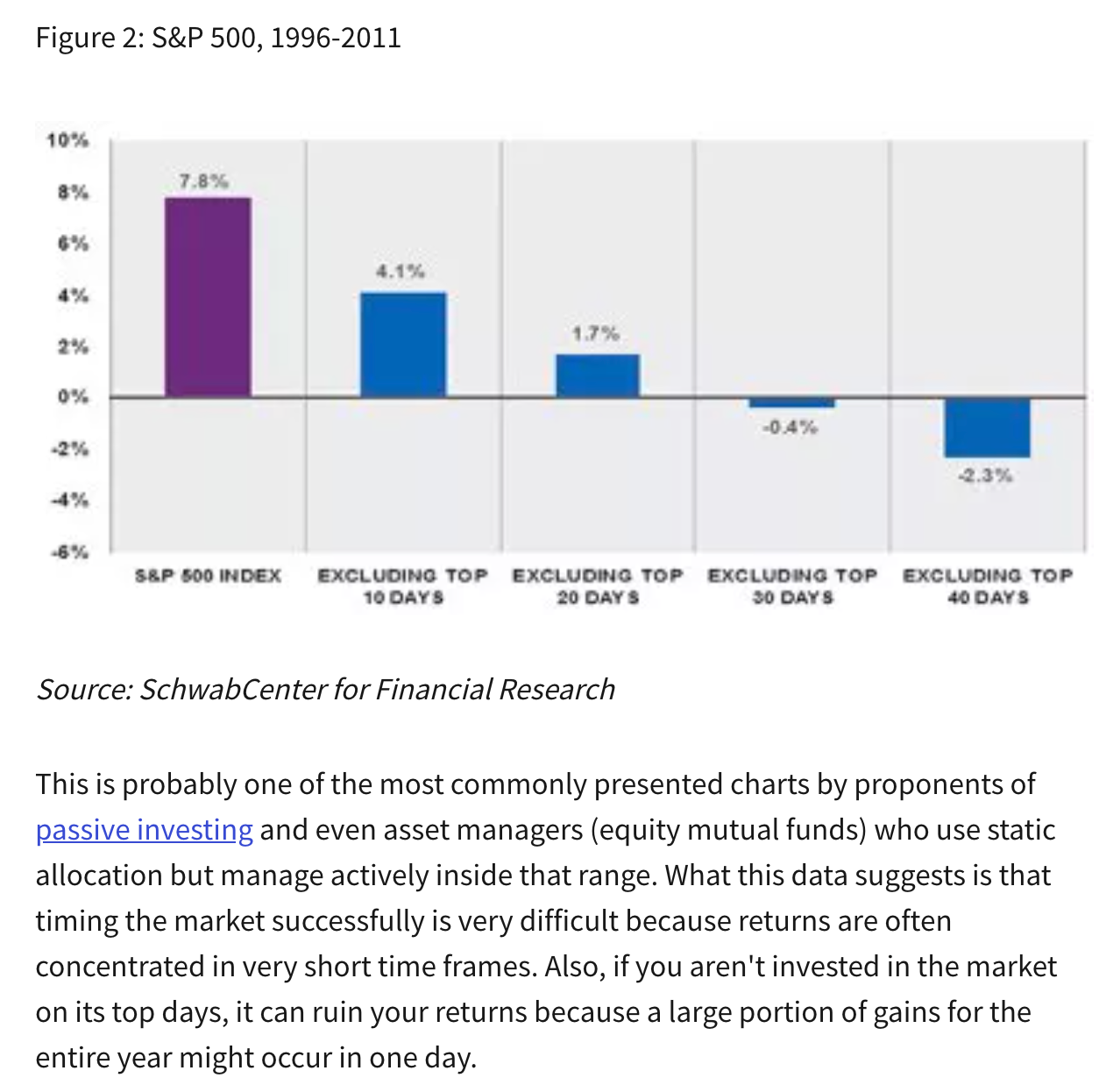

Basing your investments on “timing the market” is a huge roll of the dice. For instance, if you had missed just 10 of the top trading days from 1996 to 2011, your investment returns would have been cut in half: from 7.8% to 4.1%. That’s a huge price to pay. By contrast, investing in long-term index funds enables you to capture the market’s natural wins and losses and avoid the stupid mistakes of emotional investing.

Trying to day-trade stocks to make extra money is one of the dumbest things you can do with your finances. Don’t be swayed by the appeal of fast, flashy returns.

7. Be Leary of Financial Experts

There’s a lot of financial advice out there, but it’s not all beneficial. Before you try a new investment strategy or open a new account somewhere, know from whom you’re getting your financial tips. What are their motives? What’s their experience? What are they selling? Are they selling insurance or are they a fee-only financial planner?

A financial advisor is not the same as a Certified Financial Planner™ professional. A CFP® holds the highest possible designation for financial planning and has a fiduciary responsibility to act in their client’s best interest. While a CFP® is held to this standard, not everyone is, so be careful whose advice you take.

Anyone can designate themselves as a “financial expert.” If you come across this phrase, pause and ask yourself, “Are they selling me something? What value do their words hold? Can I learn this information for free?”

Of course, it’s important to invest in yourself by learning from others’ experiences. I, too, take courses all the time to learn new things, but I’m always cautious of pop-up entrepreneurs and so-called “financial experts” who promise big results without a certification to back them up.

You can trust that I won’t recommend something unless I’ve used it or wholly believe in the product. Investing isn’t all about throwing caution to the wind and taking big risks; sometimes caution proves more prosperous, especially when taking advice from a “financial expert.”

8. Get term Life Insurance

Compared to thrilling financial investments, insurance is boring. But to be honest, your insurance should be boring and not complicated by a bundled investment you think is a steal. I’ll give you an example.

One of the most fundamental insurance policies you need is life insurance, and it comes in a few different options. The two basic options you’ll likely find are term and whole life insurance. Which should you buy? In brief, buy term life insurance – and the earlier in your career, the better.

A term life insurance policy is something you pay for temporarily, usually for 10 to 20 years – the “term” of your policy. If you die during that term, your beneficiaries receive a life insurance payout. The amount of the payout is contingent on the amount of term insurance you purchased, such as a $100,000 policy or one that pays 1 million dollars; but either way, your beneficiaries receive the full amount in the event of your death.

Steer Clear of Permanent Life Insurance

The purpose behind life insurance is to take care of your beneficiaries, pay off your home, cover immediate expenses of your estate, and maybe help pay for your children’s education. Where it gets messy is when insurance salespeople try to sell you whole life insurance, also called permanent life insurance.

These plans are notorious for being expensive and confusing, with high premiums to pay until you die. Some salespeople will try to persuade you to buy a whole life plan with built-in retirement savings mixed into one fancy little product.

Please don’t fall for this pitch. Keep your investments and insurance separate. If someone is trying to mix the two and convince you that it’s a smart financial move, run.

In keeping with tip #7, be leary of a financial advisor or salesperson pushing a permanent (whole life) insurance plan. Generally speaking, a salesperson doesn’t have your best interest in mind. Rather, they may be after the high commission rate they’ll receive for selling the plan to you.

Don’t take the advice of an uncertified financial advisor, and don’t feel pressured to do business with a pushy salesperson; say thank you and move on.

Instead, on your own time, look at Term4Sale.com; you can find an inexpensive term life insurance policy without worrying that you’ll get hosed by an insurance salesperson. And no; I’m not affiliated with them. I used this site recently to purchase additional term life insurance for myself and my wife. I can attest that it was relatively cheap and really easy to do – even boring, as insurance plans should be.

9. Track Your Numbers

You can’t be financially savvy if you’re not financially organized. It’s essential that you keep track of your money – not just your account totals but all your numbers such as your net worth, credit score, and even retirement account fees. You’ve gotta know those numbers and look at them at least once or twice each year.

I track my numbers with Personal Capital but also recommend tools like Mint and YNAB to track numbers automatically. You don’t need to obsess over these figures, but you shouldn’t ignore them either. You can’t expect to have success in your money management, debt payoff, or investment accounts if you aren’t aware of how your numbers are changing.

To get started with tracking your numbers, take a look at these helpful tools for now. In the future, I’ll show you how to reduce unnecessary fees and improve your credit score and net worth.

The Best of All Financial Tips: Keep It Simple And Steady

Overall, the best financial tip is to keep things simple. If an investment scheme sounds too good to be true, it probably is; expect wealth to take a long time to build.

Insurance should be boring. Investing should be boring; the old adage of “slow and steady wins the race” is true of investing. But remember, investing is only one component of your financial picture, and only one tip out of the 9 covered in this post. You’ll get your best ROI from a comprehensive approach to financial health.

By following these financial tips, you’ll optimize your income, decrease debt, build your net worth, and create smart financial systems that ultimately improve your financial health. Don’t forget to keep track of your progress, and feel free to download my worksheets to help you do so.

Bonus Tip: 5 Financial Books You Need to Read This Year

If you’re looking to increase your financial literacy this year, check out these 5 financial books that I absolutely love. Two of them are classics, and although the other three are (relatively) recent releases, I consider them future classics in the personal finance canon.

1. The Next Millionaire Next Door by Sarah Stanley Fallaw and Thomas Stanley

This first book is a new take on a 1996 classic called The Millionaire Next Door written by Dr. Thomas Stanley. In this 2020 update, Dr. Sarah Stanley Fallaw expands on her father’s book with new research on the surprising truths about America’s modern millionaires.

One tidbit I love about this book – and its original – is the distinction Stanley makes between the wealthy and the rich. Frankly, anyone with a high income can be considered “rich” – the term is actually very subjective. For instance, the median salary among working adults in the US is $68,000 annually; however, physical therapist wages range from $75-100k a year. Does that make a group of professional PTs “rich”? Based strictly on the numbers, maybe so – but most of them certainly don’t feel rich.

A higher-than-average salary doesn’t make you wealthy because, as the book explains, wealth isn’t strictly dependent on income. Although a high income can help you build wealth, it’s possible – even common – to live paycheck-to-paycheck despite earning $75k, $100k, or even $200k each year.

In The Next Millionaire Next Door, Stanley Fallaw uses current research to shed really fascinating light on the behavior of millionaires. These aren’t people who caught a lucky break or inherited an estate; they’re people like you and me who learned to grow their wealth despite earning an average income. The median annual income among the millionaires featured in this book was $89,167, not far off from the typical salary of physical therapists.

So if you’re curious about how you can become the “next millionaire next door” while earning an average income, then this book is an absolute must-read.

2. The Psychology of Money by Morgan Housel

I finished this book in just a few hours, for a couple of reasons: it’s a relatively short read and it’s absolutely fascinating. Released in 2020, this book covers an extensive history of human behavior in wealth and finances.

Similar to The Millionaire Next Door, Housel’s The Psychology of Money dispels the myth that to become wealthy you need to earn an advanced degree and generate a high income. That’s just not true. As you read this book, your views on money will be transformed by the stories and examples Housel shares. From saving to investing to building wealth, The Psychology of Money will reframe how you think about finances in a way that can’t help but influence your behavior.

3. Total Money Makeover by Dave Ramsey

Ramsey’s Total Money Makeover is a personal finance classic and one I repeatedly recommend. Now as far as the author’s concerned, you either love him or hate him – but no one can deny that Dave has found a foolproof method for getting people out of debt and on the path to wealth.

Recently I came across Dave Ramsey’s YouTube channel, on which he shares much of the same practical advice from his book. No matter the platform, he peppers his pitch with success stories and motivating examples of people who got out of debt using his 7 “baby steps.” So if you have debt but don’t know where to start, pick up his book or check out his YouTube channel.

The motivation alone is definitely worth the 10 bucks you’ll spend on this book, especially if you’re interested in rehabilitating your personal finances and repaying debt.

4. The Little Book of Common Sense Investing by Jack Bogle

It may be a short work with an unassuming title, but The Little Book of Common Sense Investing is the brain-child of investing legend Jack Bogle, founder of Vanguard and key leader in the personal finance industry.

I couldn’t recommend this book enough, both for new investors and for experienced investors who want to grow their wealth. Literature like this is sorely needed right now. When it comes to investing and speculation, there is no shortage of bad advice out there. This book shows that, in the long run, investing goes beyond picking stocks or trying to find the winners and forgetting the losers. As Bogle explains, index funds typically outperform 80% of active funds and give the average investor just as much of a chance at better returns.

I discuss index funds elsewhere, but they are also propounded by investors like Warren Buffett and Charlie Munger. Yet, Bogle’s book is way more practical than almost any finance course you’ll take. It’s a little book that yields big returns – in wisdom and in finances.

5. I Will Teach You to Be Rich by Ramit Sethi

The last on our list of must-read financial books originally came out about 10 years ago but was recently updated. The author, Sethi, is one of the most down-to-earth financial writers you’ll find, lending a sense of genuineness to his book.

What I love about I Will Teach You to Be Rich is the framework Sethi uses: his personal experience. Sethi draws on his background in psychology to promote conscientious spending. This book is worth its price, if nothing else, for the included scripts to follow when asking your bank or credit card company to lower fees and waive late charges. Not only is the book relatable, readable, and smart, it’s immediately applicable to daily life.

How to Get these Financial Books: Conclusion

All of these books belong on the top shelf of your personal finance library. Commit to reading even just one or two financial books every year, and you’ll be on your way to improving your financial health for years to come.

Last I checked, you can get all these titles for less than $70 on Amazon. Dollar-for-dollar, reading each of these books is the easiest investment you can make towards learning about personal finance from some of the biggest leaders in the industry.

For an even sweeter deal, sign up for Audible through this link, where you can access these books for free as audiobooks. For over 10 years, I’ve used Audible to listen to books while driving or when working around the house. So even if you don’t have the time to sit down and read a book, you can probably accommodate listening to one on your daily commute.

There you have it – 5 excellent financial books to read this year, and an inexpensive and convenient way to consume them. What do you have to lose?