Physical Therapy liability insurance is designed to provide professional liability coverage in the case of a malpractice lawsuit. In other words, if a lawsuit is brought against you as a PT for a number of valid reasons, your Physical Therapy liability insurance will stop these claims from jeopardizing your career.

The short story: You should seriously consider liability insurance if you are a Physical Therapist.

Why Do I Need Physical Therapy Liability Insurance?

Unless you are independently wealthy enough to cover the potential costs of court fees and indemnity claims, you should probably look into malpractice insurance. The average payout for an indemnity claim made against a PT was $99,122 according to an HSPO report. Such a hefty malpractice claim could seriously hurt the average Physical Therapist, both professionally and financially.

But if my employer provides malpractice insurance, do I need personal malpractice insurance as a Physical Therapist?

That’s a good question to ask your lawyer, who will probably charge you a minimum of $150/hour to discuss it. A financial or legal professional can also discuss with you, for a fee, the details of an insurance policy in order to verify you have the most appropriate coverage.

My advice is free: it’s worth getting a personal policy. I have kept personal liability insurance as a Physical Therapist for the last 2 years by paying roughly $185/year (more on that later).

But no matter which provider you choose, the cost of professional liability insurance for PTs is very, very reasonable compared to our physician friends who pay upwards of $10,000, $50,000 and sometimes more than $100,000 a year for malpractice insurance.

For me personally, paying less than $200 a year for professional liability insurance is a no-brainer.

Do I Need Liability Insurance If I Work In A Clinic?

It’s possible for a clinic to establish a separate policy that protects its staff for potential lawsuits made against the clinic or employee. Contacting a reputable insurance company to provide a quote for your clinic is one way you can compare the policy coverage and costs associated with this type of protection.

While you could go this route, I’d recommend spending that time instead researching a personal liability insurance policy.

What About PT Students? Do They Need Professional Liability Insurance?

Most Physical Therapy programs require or even provide liability insurance for students to protect them while on clinical rotations on campus or at outside clinics. The premiums for students are typically very affordable, as low as $35/year with some insurance providers. Because lawsuits can certainly involve students, obtaining appropriate coverage and liability protection is a must for PT students.

Common Reasons for Claims Against a Physical Therapist

Still don’t think it’s necessary? Let’s take a look at the research.

A CNA/HPSO report recorded 477 claims of physical therapy malpractice were made between 1/1/01–12/31/11. That total has likely doubled, considering that a recent subset of data from a shorter period of time (1/1/10–12/31/14) reported 443 claims of physical therapy malpractice. (These would be closed claims amounting to more than $10,000.)

Considering this proportional increase in claims, it’s fair to surmise that PT malpractice lawsuits are on the rise, as well as your likelihood of getting sued.

But what kinds of claims might you be up against?

Here are the 9 commonest types of malpractice lawsuits and the average amount of indemnity paid per claim:

| Claim Type | Avg. Indemnity |

| Failure to properly test or treat a patient | $292,500 |

| Equipment-related closed claims | $127,448 |

| Improper performance of manual therapy | $126,629 |

| Failure to supervise or monitor | $109,678 |

| Improper management over the course of treatment | $104,636 |

| Improper performance using therapeutic exercise | $93,238 |

| Environment of care | $90,639 |

| Improper behavior by practitioner | $79,833 |

| Improper performance using a biophysical agent | $48,266 |

| Overall average paid indemnity | $99,122 |

A personal liability insurance policy can protect you from these claims and their indemnities. I don’t know about you, but with the number of physical therapy malpractice claims possibly on the rise, I wouldn’t want to risk having to pay out $100k – or more.

What To Look For In Physical Therapy Liability Insurance

Coverage varies depending on the provider. Generally, you’ll want to look for these types of coverage:

- Professional Liability Coverage

- License Coverage

- Lost Wages Coverage

- Deposition Coverage

- HIPAA coverage

- Assault Coverage

- Personal Injury Coverage

- First Aid Coverage

As well as the following:

- Medical Payment

- Property Damage

- Sexual Misconduct or Abuse

- Defense Attorney Provision

- Option for portability

Understand the Difference: Occurrence vs. Claims-made Coverage

As you shop for liability insurance, you may come across two options: Occurrence or Claims-made coverage. While each policy’s details may differ, there are two key distinctions in coverage which you should know.

Occurrence Coverage: This policy protects you from claims made for an instance during which you were insured, regardless of when the claim is made.

Claims-made Coverage: This policy also covers claims made for an instance during which you were insured; however, for it to protect you, your policy must still be active when the claim is made.

Breakdown of A Physical Therapy Liability Insurance Policy

Let’s take a look at a sample offering for Physical Therapy professional liability insurance.

Joe P. Therapist receives a certificate of insurance showing the following: $1,000,000/$3,000,000 for $185 per 12-month period.

The first number ($1,000,000) is the amount of coverage per occurrence or claim. The second number ($3,000,000) is the amount of total coverage available per year. Lastly, $185 is the annual premium he pays for this coverage.

What exactly does that mean for Joe? We can break it down even more.

Professional Liability Limits

The coverage for Joe’s Professional Liability policy includes protection in the following instances: “Good Samaritan liability,” “Malplacement liability,” and “Personal Injury liability.” The numbers above tell us that, with this policy, Joe is covered up to $1,000,000 per claim with a $3,000,000 aggregate for instances related to these liabilities.

Coverage Extensions

Joe P. Therapist’s coverage also extends to other major categories, including the following: License Protection, Defendant Expense Benefit, Deposition Representation, Assault, Medial Payments, First Aid, Damage to Property or Others, and Information (HIPAA) Fines. Many of these categories denote a cap, however, ranging from $10,000–$25,000.

Certificate of Insurance

A certificate of insurance serves as the proof of payment and coverage. As long as Joe P. Therapist makes his premiums every year, his certificate will be valid, and he will be covered. (The biggest mistake made by PTs seeking liability insurance is allowing their coverage to lapse!)

Is Professional Liability Insurance Worth It?

That’s a good question… I’ll ask it another way: Is it worth spending a couple hundred dollars (or less) each year for protection against license suspension, probation, revocation of your license, or losing your Physical Therapy job altogether?

Or ask yourself this: Which will cost more, $200 for professional protection or $3,000,000 in lawsuits?

I certainly think a personal policy is worth it, and I’ve even done some of the legwork for you in researching the best deals for physical therapy liability insurance.

Where to Find Liability Insurance for Physical Therapists

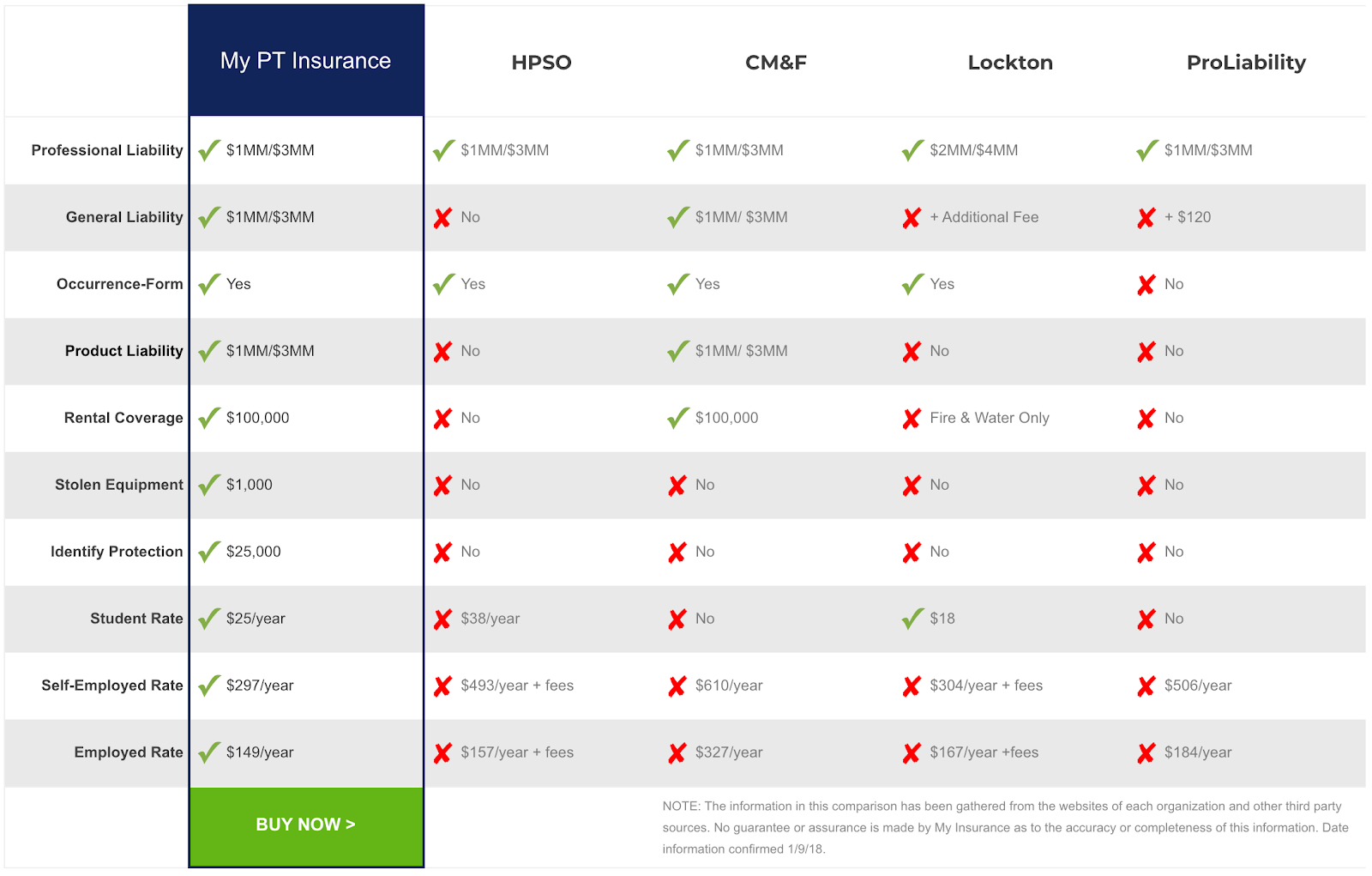

One of the most widely-used providers of physical therapy liability insurance is HPSO, which partnered with APTA back in 1992. Although it’s the insurance provider of choice for over 79,000 active PTs, it’s not necessarily the best deal.

After using HPSO as a new graduate, I found better coverage through MyPTInsurance.com.

This chart illustrates why MyPTInsurance is the best choice among leading liability insurance companies:

Like with most insurance products, it’s good to compare policies. Don’t be afraid to request quotes from multiple insurance companies so you can compare the coverages and premiums. Just because your provider is reputable doesn’t mean your coverage is adequate or fairly priced.

Ultimately, getting covered (and staying covered) is up to you. With MyPTInsurance, less than a couple hundred dollars each year will protect you from lawsuits that could possibly ruin your career.